What's Moving Markets

What's Moving Markets

Nominal Growth Remains Robust

This publication is a short excerpt from our weekly Prometheus ETF Portfolio note. While we reserve our forward-looking views on macro and portfolio construction to paid subscribers, we offer our high-level diagnostic of macro conditions here as we aim to offer value to the broader public.

For those unfamiliar: The Prometheus ETF Portfolio aims to allow everyday investors to access an investment solution that combines active macro alpha, passive beta, and strict risk control, all in an easy-to-follow, low-turnover solution. We aim to achieve strong risk-adjusted returns relative to cash, with limited capital drawdowns in depth and duration. We do this in a highly accessible package, which rotates between five highly liquid ETFs, readily available to any investor with a brokerage account. You can sign up for it here:

Let us dive into our assessment of macroeconomic conditions:

Markets moved to price in higher nominal growth and elevated liquidity conditions.

Economic data momentum moderated, once again driven by manufacturing-sensitive areas of the economy.

Real GDP conditions remain elevated relative to recent history, supporting risk assets.

Let's dive into the data driving our assessment before moving on to positioning. We begin by examining the path of asset price returns over the last week:

As we can see above, commodity prices offered the smoothest path of returns, along with the highest risk-adjusted returns. This pricing came as economic data momentum fell significantly this week:

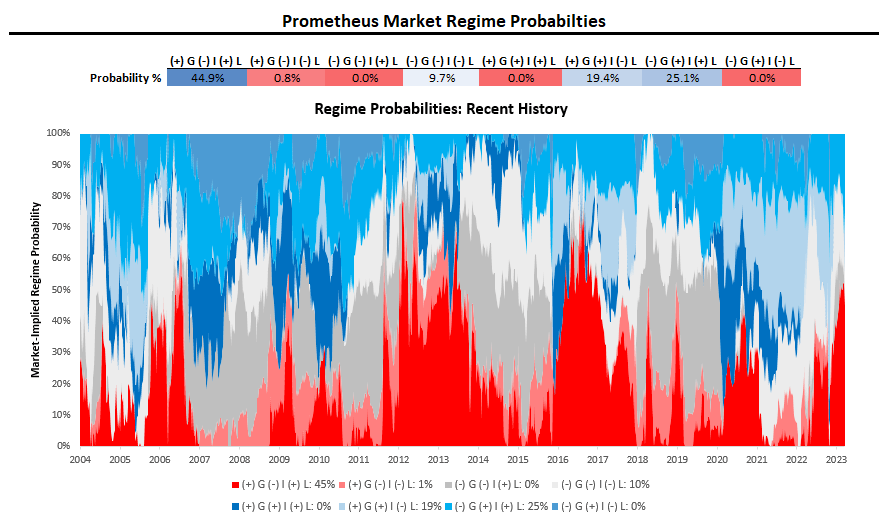

This weakness in economic data momentum was once again driven by manufacturing-sensitive areas of the economy, i.e., capacity utilization, PMIs, and retail sales. This is the second consecutive week of data weakness driven by the manufacturing economy. We monitor these dynamics carefully. For a further understanding of how economic dynamics have been priced into markets, we show our tracking of market-implied macroeconomic regime probabilities below, which reflect the aforementioned dynamics:

Markets continued to price regime probabilities consistent with a rising real growth and liquidity environment on a trend basis. Incrementally, markets have moved to price in higher probabilities of rising inflation regimes, consistent with the latest CPI data. Overall, we continue to remain in an environment where nominal growth conditions remain strong and recessionary pressures are low.

As we can see above, nominal GDP conditions remain elevated. We allocate accordingly. Until next time.