The Observatory

The Observatory

CPI Review: Slowdown Pressures Manifesting

Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

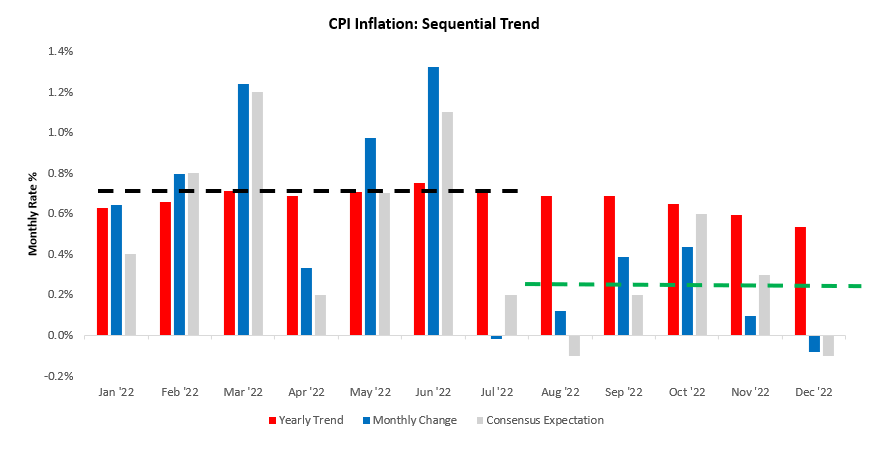

CPI inflation came in line with consensus expectations but counter to our forecasts. CPI Inflation decreased -0.08% in December. This print contributed to a sequential deceleration in the quarterly trend relative to the yearly trend. Below, we show the monthly evolution of the data relative to its 12-monthly trend and consensus expectations:

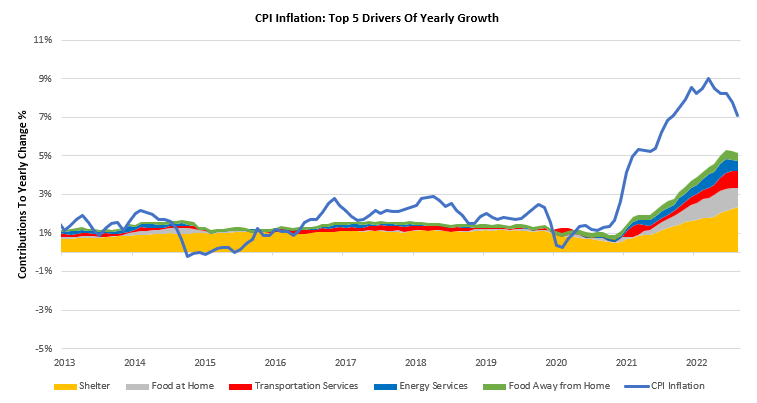

Over the last year, Food at Home (1%), Food Away from Home (0.43%), Energy Services (0.55%), Shelter (2.46%), & Transportation Services (0.88%). have been the primary drivers of the 6.42% CPI inflation. We show the contributions of these items to yearly changes in total spending below:

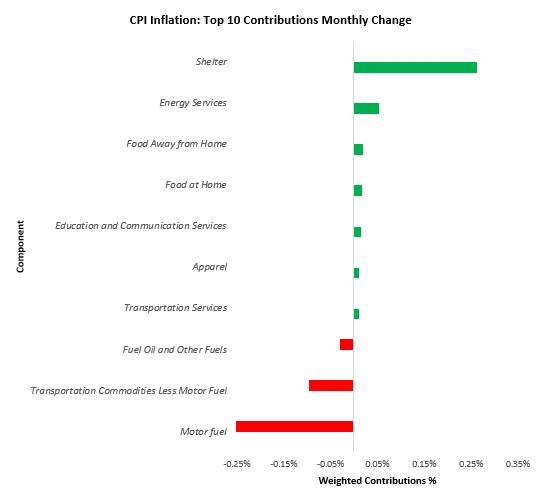

Of particular note in this release was the severity of energy deflation. Additionally, we saw extremely strong pressure coming from transportation commodities, ex-motor fuel:

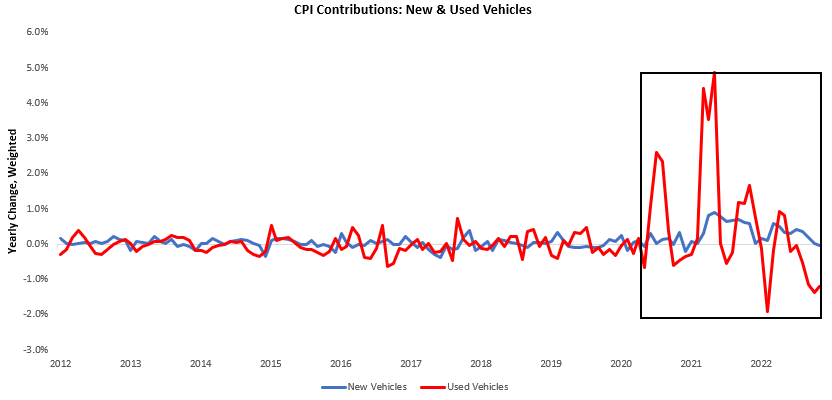

Within this category, used cars continue to be the primary driver of declines; however, new cars have also now slipped into deflation. We show this below:

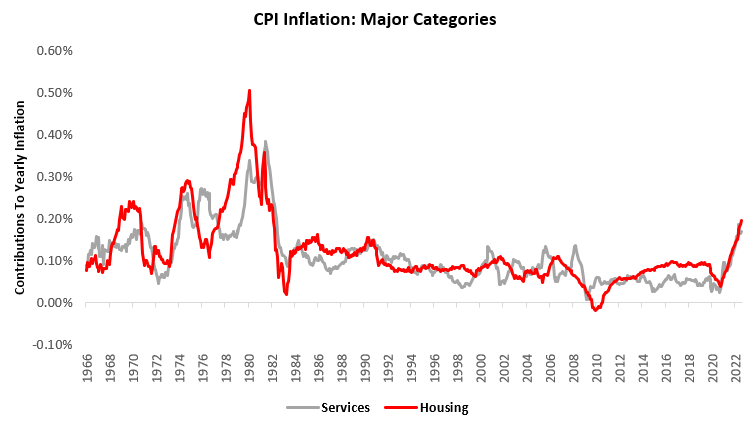

The themes we highlighted in our Month In Macro report remain intact, i.e., divergences between the goods and services economy continue to persist. Below, we show the yearly change in services inflation:

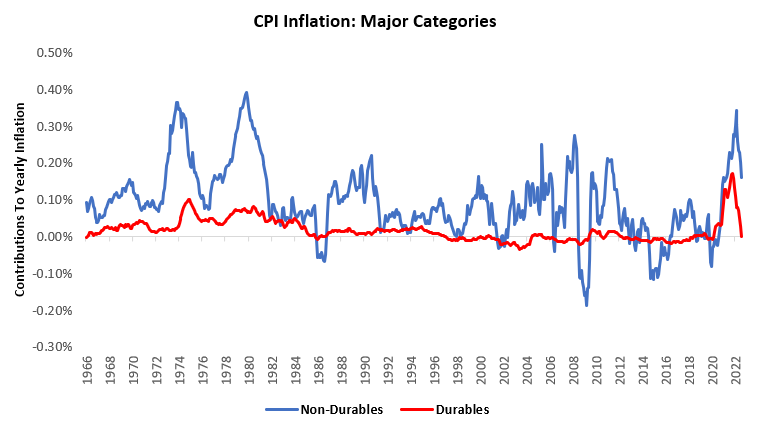

In contrast, the goods economy continues down a deflationary path:

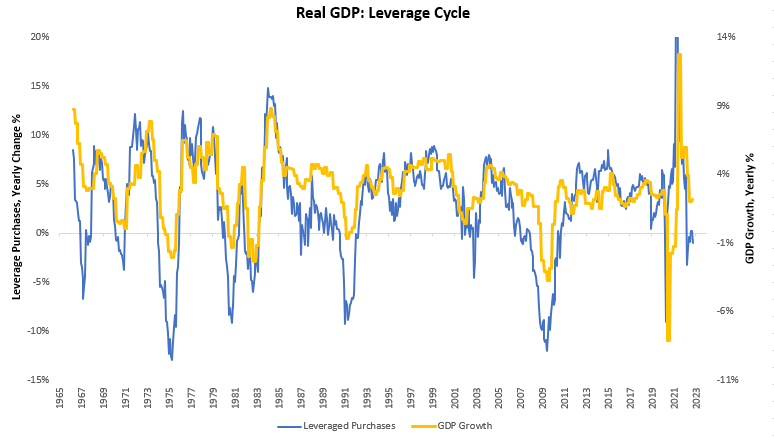

This divergent rate of inflation is largely a function of the slowdown elicited by Federal Reserve policy. We are seeing the cyclically sensitive, leveraged sector of the economy weakening faster than the service-oriented, income-sensitive sectors. We see this in our tracking of the leveraged sectors of the economy:

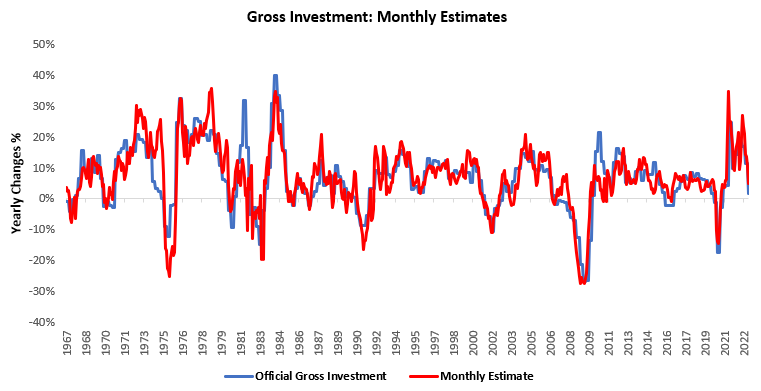

We see this further in our tracking of nominal investment, which is primarily driven by real estate & equipment investment:

Overall, the cyclical slowing of the economy via tighter liquidity conditions continues to pressure nominal and real activity, creating deflationary pressures. These exist alongside inflationary pressures in the services economy. The combination of these competing forces continues to force of stabilization of inflation at a high level. The next stage of the cycle will be determined by whether the recessionary & deflationary pressures in the goods economy will be enough to bring down nominal income and spending on services. This is another step forward in the slowdown. Until tomorrow.

As per my comment on TW, really appreciate your openness and quick turnaround in terms of analysis and commentary pre- & post- key events like CPI updates. Really helpful for readers (like me!) to learn more.

I do wonder if inflationary contribution by services will begin to ease off as well. Demand for services picked up as the world opened up again but we're seeing tech layoffs come full swing and this could work it's way through the rest of the services industry and reduce tightness perhaps?

Thank you for the comments. Do you have a model outlining your expected path for employment, and if so, what does it suggest regarding coming pressure (or not) on nominal income and spending on services?