The Observatory

Click here to enter The Observatory.

The Observatory is how we systematically track the evolution of financial markets and the US economy in real-time. Without further ado, let’s dive into what our systems are telling us:

Markets:

Yesterday, market pricing offered opportunities to reduce exposure to Commodities, both on the Alpha and Beta sides. Equity Markets bounced, creating the chance to add to shorts in Communications on Consumer Discretionary Sectors. We should note there is a high and rising probability of risk-off regime, i.e., (-) G (+) I and (-) L. While in the current market regime, selective equity shorts are warranted, outright equity shorts come into play in either of these regimes. Therefore, equity shorts are likely to remain portfolio accretive unless market regime dynamics shift dramatically.

To summarize our systems' current assessment: Our Market Regime Monitors show that (+) G (+) I; has begun to seed ground to (-) G (+) I and (-) L this week. Our signals are beginning to price increasing odds of risk-off regimes. Equity Momentum continues to flounder, generating a poor signal for trend followers this year. Our Momentum Monitors continue to flag that cross-asset momentum favors inflation. Gold and Commodities remain well supported during both (+) G (+) I or (-) G (+) I. Our systematic forecasts point to (-) G (+) I regime, followed by an eventual transition to (-) G (-) I. Gold would be a bridge between these regimes. Consequently, our systems tell us that the best opportunities are LONG: Bonds, Gold, Cotton, Lean Hogs, Live Cattle & Sugar, and SHORT: Communications. However, our Risk Management Monitors indicate that we can ADD to LONG: Bonds, Cotton, Lean Hogs, Live Cattle, and SHORT: Communications. We can REDUCE our LONG: Gold & Sugar. Our Expected Return Strategy is LONG: Bonds, Gold, Cotton, Lean Hogs & Sugar, and SHORT: Communications.

Macro:

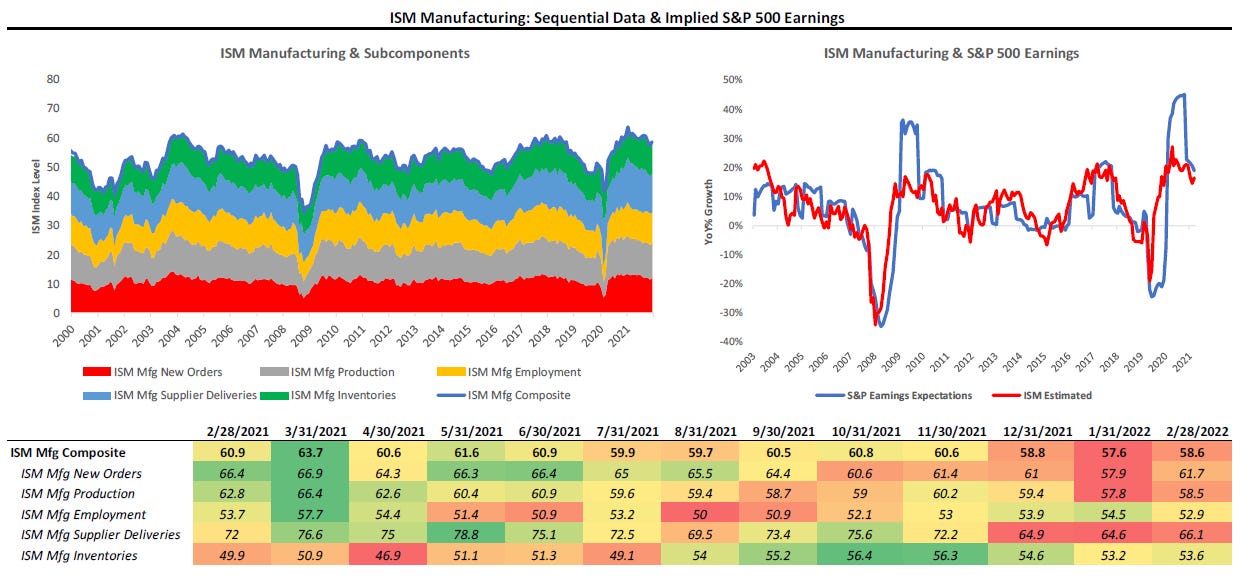

The latest ISM data allowed Economic Momentum to bounce higher; however, we think it is essential that we don't conflate sequential strength with cyclical strength at this stage in the cycle. PMI data survey respondents regarding their sequential views, i.e., relative to the previous month, and does not consider cycle dynamics. The trend remains lower.

To summarize our systems' current assessment: The latest economic data created a big move lower in our GDP Nowcast, with economic growth tracking at 1.5%. Economic Momentum widened its divergence versus the trend in economic growth after recent ISM Manufacturing data. The decelerations we have expected since Sept 2021 are now imminent on the forecast horizon. Data is likely to turn for the March-April reporting period. Our Liquidity Indices led these moves, which estimated slowdowns this year. Our Liquidity Monitor shows growth in Institutional Money Funds continued to remain weak in February. These money market funds are key players in creating funding for repo markets and other funding markets, i.e., slowdowns in these funds tend to weigh on market finance.

The future is dynamic, and our systems adjust as new information is available. Our bias is to allocate for the existing regime while trying to peek around the corner to what the future may hold. Finally, we optimize these views to minimize portfolio risk, resulting in our trading signals. We show all this in the document below.

Click here to enter The Observatory.