Month in Macro

We share a sample of our Month In Macro from October 2023. This will soon be available to subscribers as a paid subscription. Month In Macro offers the most detailed evaluation of macro drivers you will find in the industry. Every month, we assess the most important dynamics in the macroeconomy and what it means for markets. We all share systematic asset allocations coming from our quantitative process. You won’t find anything else like it:

This note aims to share our research team's internal checkpoint process in evaluating the current state of the economy as it pertains to markets. The pages that follow will have familiar content for those who follow our work, but with the added benefit of our connecting the dots across all the economic and financial data our systems use to make portfolio decisions. Our primary takeaways are as follows:

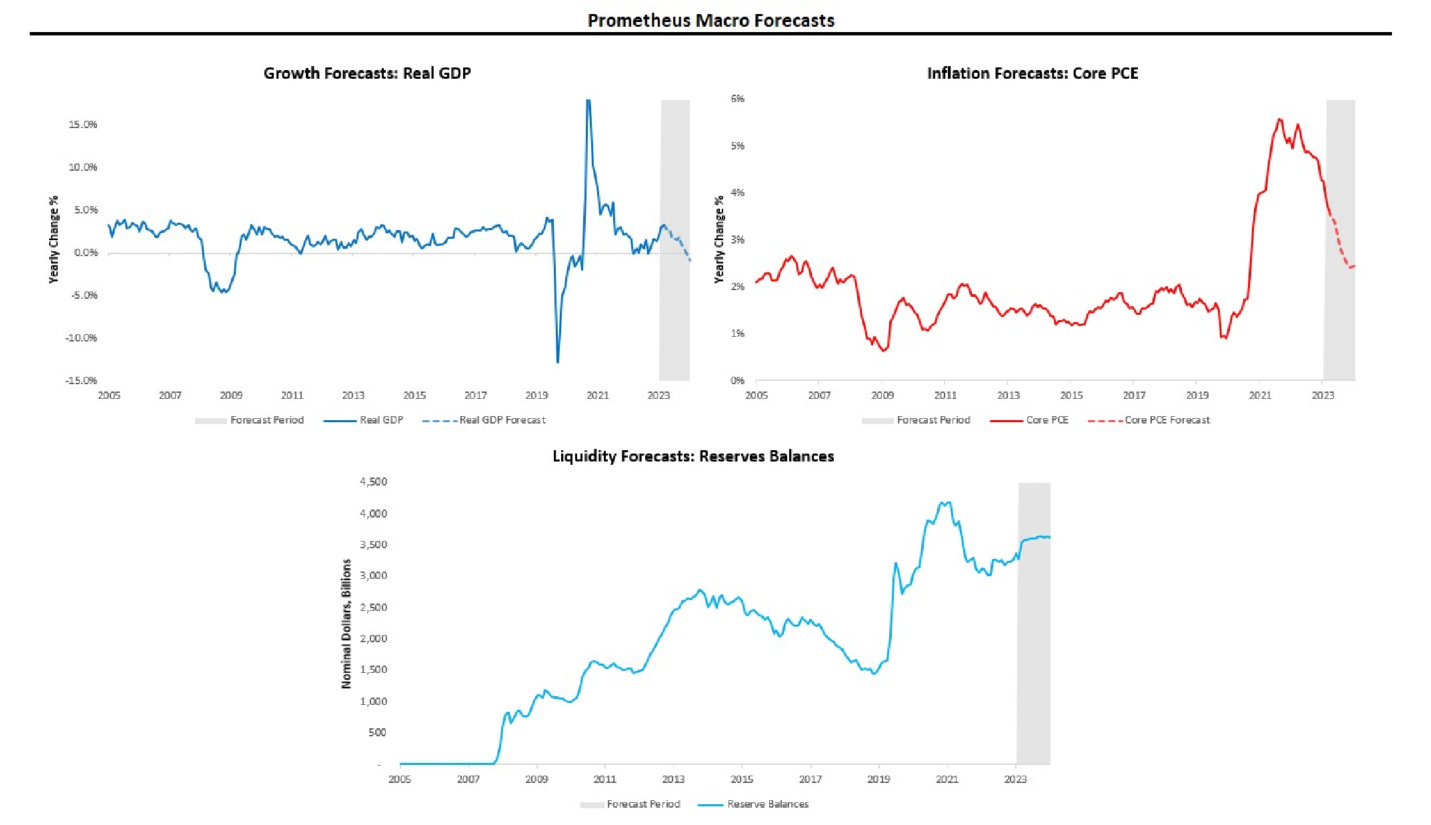

Nominal GDP contracted by -0.11% in October, with real GDP contracting by -0.24% with inflation rising by 0.13%. Meanwhile, despite ongoing QT, reserve balances in the financial systems have continued to expand, supporting liquidity conditions.

Cyclical dynamics and our outlook on nominal activity have begun to shift. While our expectations for real growth remain that they will soften, conditions are now aligning for inflationary pressures to abate, potentially pushing us out of an inflationary bear market.

We are at what resembles a turning point for treasury markets, with the amelioration of short-rate pressures and declining inflationary forces. The end of short-rate pressures are more apparent than decreasing inflationary forces.

After losses across positions last month, our Cycle Strategies are flat stocks & bonds and long commodities.

Please find the full report below.