Month in Macro

We share a sample of our Month In Macro from October 2023. This will soon be available to subscribers as a paid subscription. Month In Macro offers the most detailed evaluation of macro drivers you will find in the industry. Every month, we assess the most important dynamics in the macroeconomy and what it means for markets. We all share systematic asset allocations coming from our quantitative process. You won’t find anything else like it:

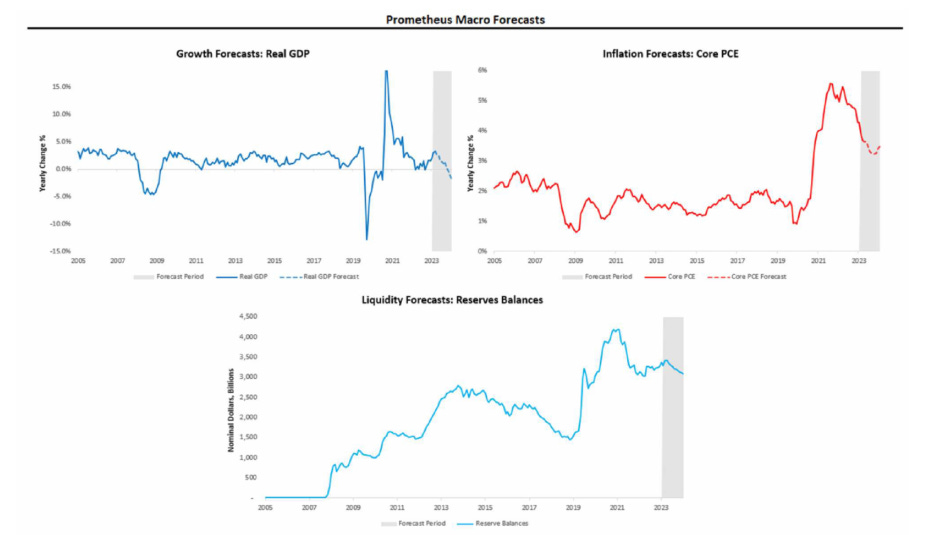

This note aims to share our research team's internal checkpoint process in evaluating the current state of the economy as it pertains to markets. The pages that follow will have familiar content for those who follow our work, but with the added benefit of connecting the dots across all the economic and financial data our systems use to make portfolio decisions. Our primary takeaways are as follows:

Nominal GDP expanded by 0.66% in September, with real GDP increasing by 0.38% and inflation rising by 0.28%. Meanwhile, despite ongoing QT, reserve balances remained flat during the same period.

Most recent employment data shows signs of weakness driven by manufacturing weakness. We think this can continue, but not at the current pace. Until nominal activity declines meaningfully, we will remain in an inflationary regime.

Cross-currents from policy winds coming from the Fed and Treasury continue to blunt the tightening of financial and economic conditions. We expect these cross currents to keep liquidity at a high level.

After making all-time highs last month, our Cycle Strategies remain short stocks, short bonds, and long commodities.

Please find the full report below.